A ranked guide to the TIC industry’s global leaders: revenue, headcount, market valuation, and what each one is best known for.

The Testing, Inspection and Certification industry sits at the intersection of trade, safety and trust. Every container that crosses a border, every car that comes off a production line, every food product on a supermarket shelf, every wind turbine raised offshore, and every pharmaceutical batch released to patients passes through a TIC company at some stage.

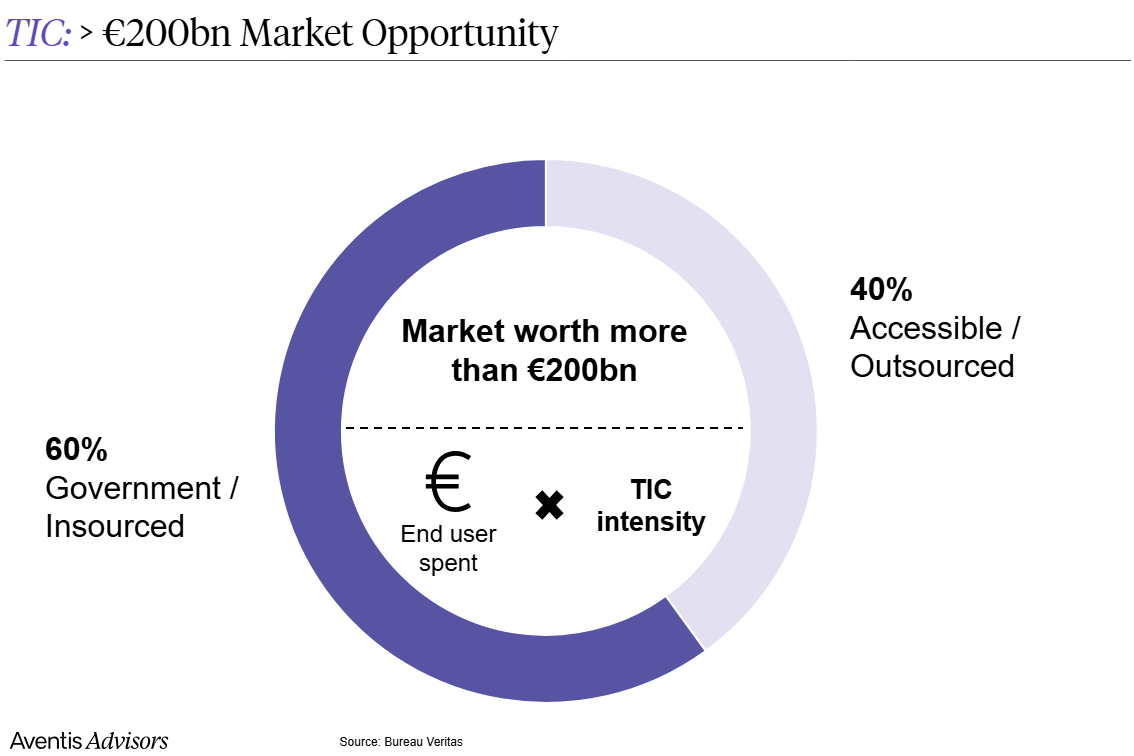

The global TIC market is worth more than EUR 200 billion today and is expected to grow at 4 to 5% per year through the end of the decade, driven by tightening regulation, the energy transition, supply-chain reshoring, and the digitalisation of compliance.

Despite the size of the prize, the industry remains remarkably fragmented. The top ten players together control less than a quarter of global revenue, and the long tail is filled with thousands of specialist laboratories serving local markets and niche verticals.

Below we rank the ten largest TIC companies in the world by revenue, look at how the listed players are valued on public markets today and present short profiles of the leading firms.

Industry context

The modern TIC industry was born in the 19th century to certify cargo for global shipping. Bureau Veritas (1828), ALS (1863), TÜV SÜD (1866), TÜV Rheinland (1872), SGS (1878) and Intertek (1885) all trace their roots to that era. The underlying business model has barely changed in 150 years: independent third-party experts physically test, inspect or audit an asset, then issue a report that regulators, insurers or customers can trust.

What has changed is the scope. Today’s TIC majors cover everything from commodity assays in Australian mining pits to cybersecurity certification of connected medical devices in Silicon Valley. Roll-up M&A has accelerated since 2015, with private equity injecting capital into mid-market specialists. The result is a small set of global giants flanked by hundreds of attractive acquisition targets, exactly the dynamic that makes TIC one of the most active sub-sectors in business-services M&A today.

Top 10 TIC companies by revenue

The table below ranks the ten largest TIC companies in the world by full-year revenue (latest available financials, converted to USD). Together they generate close to USD 50 billion of revenue and employ more than 450,000 people across more than 140 countries.

| # | Company | Country | Revenue (USD m) | Employees |

|---|---|---|---|---|

| 1 | SGS SA | Switzerland | 8,758 | ~99,250 |

| 2 | Eurofins Scientific | Luxembourg | 8,567 | ~62,000 |

| 3 | Bureau Veritas | France | 7,845 | ~84,000 |

| 4 | DEKRA | Germany | 5,045 | ~49,000 |

| 5 | Intertek Group | United Kingdom | 4,619 | ~44,000 |

| 6 | TÜV SÜD | Germany | 4,029 | ~28,000 |

| 7 | TÜV Rheinland | Germany | 3,189 | ~21,000 |

| 8 | UL Solutions | United States | 3,106 | ~15,500 |

| 9 | Applus+ | Spain | 2,418 | ~24,000 |

| 10 | ALS Limited | Australia | 2,113 | ~22,000 |

Valuations of listed TIC players

Six of the top ten are publicly listed. Their enterprise values and trading multiples (as of May 2026) are summarised below. Listed TIC companies trade at a median EV/EBITDA multiple of around 12x, with premium operators such as UL Solutions and ALS commanding multiples well above 18x. For a more detailed view of TIC valuations, see our related article.

| Company | Ticker | EV (USD m) | EV/Revenue | EV/EBITDA |

|---|---|---|---|---|

| SGS | SWX:SGSN | 24,911 | 2.8x | 13.8x |

| UL Solutions | NYSE:ULS | 20,543 | 6.6x | 25.6x |

| Eurofins Scientific | ENXTPA:ERF | 16,609 | 1.9x | 8.7x |

| Bureau Veritas | ENXTPA:BVI | 15,581 | 2.0x | 9.8x |

| Intertek Group | LSE:ITRK | 12,128 | 2.6x | 11.7x |

| ALS Limited | ASX:ALQ | 9,329 | 4.4x | 18.3x |

DEKRA, TÜV SÜD and TÜV Rheinland are foundation-controlled and not publicly traded. Applus+ was taken private in 2024 by Apollo and I Squared Capital.

Growth and margins

A TIC business is fundamentally a people business: labs, inspectors, engineers, auditors, so margin discipline is the single most important indicator of operational quality, and growth is the best indicator of strategic positioning. The table below compares the latest reported revenue growth and EBITDA margin for each of the top ten players, sorted by margin.

| Company | Revenue growth | EBITDA margin | Gross margin |

|---|---|---|---|

| UL Solutions | 6.9% | 22.8% | 49.9% |

| Intertek Group | 1.1% | 21.8% | 56.9% |

| ALS Limited | 18.2% | 20.6% | 29.3% |

| Eurofins Scientific | 5.0% | 19.9% | 22.5% |

| Bureau Veritas | 3.7% | 18.4% | 29.1% |

| SGS | 2.2% | 17.9% | 44.3% |

| Applus+ | 8.0% | 16.3% | n/d |

| TÜV Rheinland | 11.2% | 13.2% | n/d |

| DEKRA | 4.7% | 11.2% | n/d |

| TÜV SÜD | 9.2% | n/d | n/d |

Two clusters stand out. The high-margin operators — UL Solutions, Intertek, ALS, Eurofins, Bureau Veritas and SGS — all sit between 18% and 23% EBITDA margin, reflecting decades of mix improvement, pricing power in regulated services, and lab-network scale.

The pure-play product certification and consumer-products specialists (UL, Intertek) lead on gross margin thanks to recurring follow-up testing and mark licensing revenue.

The German foundation-controlled groups (DEKRA, TÜV Rheinland and TÜV SÜD) trail on profitability, partly because of their heavy exposure to capital-intensive vehicle inspection, partly because the foundation model deliberately reinvests rather than maximising margin.

On growth, the picture is different. The fastest-growing operator in the group is ALS at 18% organic and acquired growth, propelled by a strong cycle in minerals testing and a rapidly expanding environmental and food platform.

Company profiles

Each profile below covers what the company does, its geographical footprint, and the industries where it is strongest.

1. SGS SA

sgs.com

Revenue: USD 8.76bn • Founded: 1878 • HQ: Switzerland

SGS is the world’s largest TIC company and the benchmark the rest of the industry is measured against. Headquartered in Geneva, the group operates more than 2,500 offices and laboratories in 115+ countries and employs close to 100,000 people. Its work spans the full value chain: minerals and metals testing, agricultural commodities inspection, oil & gas certification, consumer-goods quality assurance, life sciences, automotive and industrial inspection. SGS has historically been strongest in commodities and trade-related services, but a steady stream of bolt-on acquisitions has built leading positions in connectivity, cybersecurity and ESG assurance.

2. Eurofins Scientific

eurofins.com

Revenue: USD 8.57bn • Founded: 1987 • HQ: Luxembourg

Eurofins is the youngest of the global majors and the only one purpose-built around laboratory testing. From a single lab in Nantes, founder Gilles Martin and his family have rolled up more than 900 sites across 60+ countries through an aggressive acquisition strategy. The group is the global leader in food, environmental, pharmaceutical and clinical diagnostic testing, complemented by fast-growing positions in agroscience, consumer products and BioPharma services. Roughly half of revenue comes from Europe and a third from North America. Eurofins remains majority-controlled by the Martin family and is listed in Paris.

3. Bureau Veritas

group.bureauveritas.com

Revenue: USD 7.84bn • Founded: 1828 • HQ: France

Bureau Veritas is the second-oldest of the global TIC majors and the most internationally diversified player in the industry. From its Paris headquarters it operates around 1,600 offices and labs across 140 countries with roughly 84,000 employees. The group is organised into six divisions: Marine & Offshore, Industry, Building & Infrastructure, Agri-Food & Commodities, Consumer Products, and Certification. With no single segment above 25% of revenue. Bureau Veritas is particularly strong in marine classification, infrastructure inspection and commodity-trade services, and has been investing heavily in services tied to the energy transition.

4. DEKRA

dekra.com

Revenue: USD 5.05bn • Founded: 1925 • HQ: Germany

DEKRA is the largest privately held TIC company in the world and Europe’s leading vehicle inspection group. Founded in Berlin as a motorists’ association, DEKRA today employs around 49,000 people across more than 60 countries. Roughly half of revenue still comes from vehicle inspection — the network performs over 30 million periodic technical inspections a year — but the group has diversified aggressively into industrial inspection, product testing, claims management, cybersecurity certification and workplace safety. Germany remains the home market, but DEKRA has built strong positions in France, Spain and the United States through targeted bolt-on acquisitions.

5. Intertek Group

intertek.com

Revenue: USD 4.62bn • Founded: 1885 • HQ: United Kingdom

London-listed Intertek is the most consumer-products-focused of the global majors. The group operates more than 1,000 labs and offices in 100+ countries with around 44,000 employees, organised into three divisions: Consumer Products, Corporate Assurance, and Industry & Infrastructure. Intertek is the global leader in soft-line and electrical-product testing for retailers and brand owners, and a top-three player in supply-chain assurance, sustainability auditing and connected-device certification. Its asset-light, services-led business model has made it one of the highest-margin operators in the industry, consistently delivering operating margins above 16%.

6. TÜV SÜD

tuvsud.com

Revenue: USD 4.03bn • Founded: 1866 • HQ: Germany

TÜV SÜD traces its origins to a Mannheim steam-boiler inspection association and remains majority-owned by a non-profit foundation. The Munich-headquartered group operates in more than 50 countries with about 28,000 employees, although Germany still accounts for roughly half of revenue. TÜV SÜD’s strongest verticals are mobility (vehicle inspection and homologation in Germany), industrial services, real-estate inspection and management-system certification. The group has been investing in faster-growing geographies (China, India and the United States) and in newer service lines around battery testing, autonomous-vehicle approval, hydrogen, and cybersecurity certification.

7. TÜV Rheinland

tuv.com

Revenue: USD 3.19bn • Founded: 1872 • HQ: Germany

Headquartered in Cologne and structured as a stiftung (foundation), TÜV Rheinland is the second of the three German “TÜV” groups by revenue. It employs around 21,000 people across 50 countries and is organised into six business streams covering mobility, industrial services, products, ICT & cybersecurity, systems certification, and training. Outside Germany, TÜV Rheinland is unusually strong in Greater China, where it is one of the leading testing partners for the electronics and solar industries. The group has been growing its US footprint via acquisitions in functional-safety, EMC and cybersecurity testing.

8. UL Solutions

ul.com

Revenue: USD 3.11bn • Founded: 1894 • HQ: United States

UL Solutions is the only American company in the global top ten and the listed leader in product safety certification. Headquartered in Northbrook, Illinois, UL began as Underwriters Laboratories to standardise the safety of electrical equipment, and the iconic “UL Mark” still appears on billions of products. Following a 2024 IPO, UL Solutions trades on the NYSE and operates more than 100 labs across 40+ countries with around 15,500 employees. The group is structured around Industrial, Consumer, and Software & Advisory segments, with leadership positions in EV batteries, building materials, appliances and connected-device certification.

9. Applus+

applus.com

Revenue: USD 2.42bn • Founded: 1996 • HQ: Spain

Madrid-based Applus+ is the youngest of the European majors, assembled in the late 1990s by combining a number of Spanish testing assets. The group employs around 24,000 people and operates in 70+ countries through four divisions: Energy & Industry, Automotive, Laboratories, and IDIADA — one of the world’s leading automotive engineering and homologation businesses. Applus+ is the global leader in non-destructive testing for the energy sector and a top operator of vehicle inspection concessions in Spain, Ireland, the United States and Latin America. The group was taken private in 2024 by Apollo and I Squared Capital.

10. ALS Limited

alsglobal.com

Revenue: USD 2.11bn • Founded: 1863 • HQ: Australia

Brisbane-headquartered ALS is the global leader in commercial geochemical analysis for the mining sector and a top operator in environmental, food, pharmaceutical and life-sciences testing. The group runs more than 350 labs across 65 countries and employs around 22,000 people. ASX-listed for decades, ALS is structured around two divisions, Commodities and Life Sciences, each contributing roughly half of revenue. Mining exposure has historically made earnings more cyclical than its peers, but a decade of acquisitions in environmental and food testing has materially improved the revenue mix and margin profile.

What this means for M&A

The TIC industry is unusual in that its leaders are mostly very old, very international, and very acquisitive. The top ten companies together generate close to USD 50 billion of revenue, employ more than 450,000 people and operate in almost every country in the world, yet none has a market share above 4%. That fragmentation is what makes the sector such a fertile hunting ground for M&A.

Public-market valuations underline the appeal. Listed TIC operators trade at a median EV/EBITDA multiple of around 12x. Private equity has been an increasingly active buyer at the mid-market end of the spectrum: Apollo and I Squared Capital taking Applus+ private in 2024 is just the most visible example, while many companies outside of Top 10 are private-equity backed: Apave, Kiwa, Socotec, Phenna, Normec, etc. Founders and family owners of specialist labs continue to find willing acquirers at attractive multiples, and the consolidation cycle shows no signs of slowing.

Methodology and sources

Revenue, EBITDA and enterprise-value figures are based on the latest available company-reported financials converted to USD, supplemented by S&P Capital IQ data as of May 2026. Employee counts are approximations drawn from each company’s most recent annual report or corporate fact sheet. Ranking is by reported group revenue.